Equifax Car Finance Checker

You may be eligible for compensation if you’ve bought a car, van, motorbike or campervan on finance between 2007 and 2024 as part of the Financial Conduct Authority (FCA) redress scheme.

12.1 million agreements nationally could be affected; check your motor finance history securely now for FREE.

For further information, please view our FAQs.

Download the myEquifax™ app today

Information correct as of 1 April 2026

Join the 28.8 million myEquifax™ users globally

across UK, USA, Canada and Australia as of March 2025

Check Your Finance History Now With Equifax

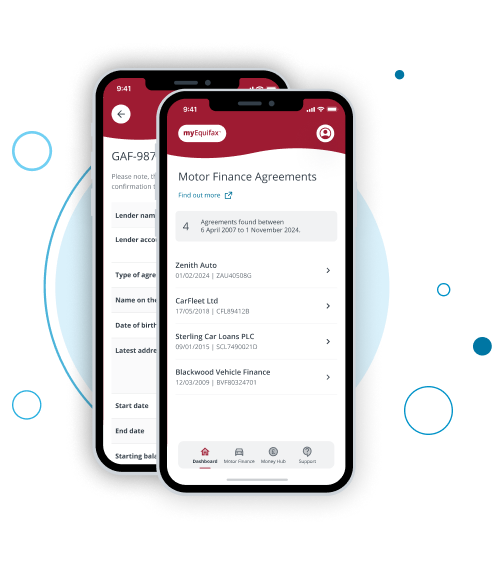

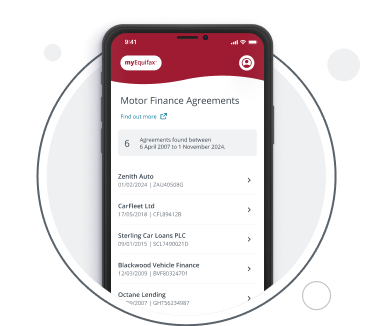

The Equifax Car Finance Checker is the safe and secure way to help you find your past or current motor finance agreements. With data going back to 2007, Equifax offers a comprehensive way to identify motor finance agreements that could be included in the upcoming compensation scheme.

The risk of fraud during schemes of this nature can increase. When searching for your motor finance history, it’s important to know who you are dealing with. With Equifax, you can trust that your personal details are safe and secure.

To access this, you just need to download the myEquifax™ app and sign up for Equifax Basic™. This will give you access to your FREE Equifax Credit Score and motor finance agreements in one place.

Once you have this information, you can raise a complaint with your lender if you wish. If you’re already signed up to Equifax Basic™ or the Equifax Credit Report & Score, you just need to download the app and sign in.

Please note: Information on your motor finance agreements in the Equifax app does not mean that you are entitled to compensation.

Download the myEquifax™ app now

Is Your Car, Van or Motorbike Finance Eligible for a Claim?

Many drivers were unknowingly charged more than they should have been due to commission arrangements between dealers and lenders. You may be eligible if:

- You financed a car, van, motorbike, or campervan (not caravans) between 6 April 2007 and 1 November 2024.

- You used PCP (Personal Contract Purchase) or Hire Purchase (HP) finance.

- You’ve since paid off the loan, no longer own the car, or even had it repossessed, you could still be eligible.

If you had multiple motor finance deals during this time, you may be eligible for multiple claims.

If you had a 0% interest deal, the FCA has confirmed these agreements are not eligible for the scheme.

Eligibility for Motor Finance Claims

The FCA’s scheme covers three categories of motor finance claims:

Discretionary Commission Arrangements (DCAs)

Contractual commission ties

High commission models

It’s important to note there are some exceptions. You should visit the FCA website for further information on the scope of the motor finance redress scheme.

How Much Compensation Could I Get?

The FCA has set out how lenders assess claims and calculate any compensation. They estimate that consumers will receive an average of approximately £830 per agreement. Please see the FCA website for further information on how compensation is calculated.

How the Equifax Car Finance Checker Works

We make it quick and easy to find your current and historical motor finance agreements.

1

Download the myEquifax™ app (available on iOS & Android).

2

Create or sign in to your Equifax account.

3

View your motor finance agreements dating back to 2007.

Even if you no longer have your car or finance paperwork, our historical data helps you identify old agreements that could be eligible for compensation.

Please note: Information on your motor finance agreements in the Equifax app does not constitute confirmation that you are entitled to compensation.

Your next step is to contact your lender(s) directly if you wish to raise a complaint. The FCA has confirmed that you do not need to use a Claims Management Company (CMC) to do this.

Motor Finance Redress Scheme

Many motor finance agreements included commission arrangements that may have led to you paying a higher interest rate than you should have.

Because of this, many motorists believe that they have been mis-sold car finance. However, the Financial Conduct Authority (FCA) states that these higher interest rates are a result of an 'unfair relationship' between the lender and the borrower.

If you bought a car, van, motorbike or campervan on PCP or Hire Purchase between 6 April 2007 and 1 November 2024, you could be eligible for the compensation scheme.

Please see the FCA website for further information on the scope of the scheme.

Please note: Information on your motor finance agreements in the Equifax app does not mean that you are entitled to compensation.

Your next step is to contact your lender(s) directly if you wish to raise a complaint. The FCA has confirmed that you do not need to use a Claims Management Company (CMC) to do this.

Take Control of Your Credit

Compare the features and benefits of the Equifax Family & Friends Plan, Equifax Credit Report & Score, and Equifax Basic in the table below.

Equifax

Family & Friends Plan

- Up to 3 users

- One digital 12 month rewards card for the main user**

- Credit score tracker

- Credit report alerts

- Credit report hints & tips

- Equifax WebDetect

- Equifax SocialScan

- Access to enhanced Equifax credit report

- Credit score updated daily

- Access to historical credit reports

- Access to Knowledge Centre

- Support from customer care team

First 30 days FREE

then £22.95 a month.

You can cancel at any time.

Equifax

Credit Report & Score

- Up to 3 users

- One digital 12 month rewards card for the main user**

- Credit score tracker

- Credit report alerts

- Credit report hints & tips

- Equifax WebDetect

- Equifax SocialScan

- Access to enhanced Equifax credit report

- Credit score updated daily

- Access to historical credit reports

- Access to Knowledge Centre

- Support from customer care team

First 30 days FREE

then £14.95 a month.

You can cancel at any time.

Equifax

Basic

- Up to 3 users

- One digital 12 month rewards card for the main user**

- Credit score tracker

- Credit report alerts

- Credit report hints & tips

- Equifax WebDetect

- Equifax SocialScan

- Access to enhanced Equifax credit report

- Credit score updated monthly

- Access to historical credit reports

- Access to Knowledge Centre

- Support from customer care team

FREE

Upgrade at any time.

*Your first 30 days are free then it’s £22.95 a month for Equifax Family & Friends Plan or £14.95 a month for Equifax Credit Report & Score. You can cancel at any time.

** Main user is eligible for one free digital 12 month tastecard. Access withdrawn upon cancellation of Equifax subscription

Car Finance Checker FAQs

You may be eligible if you took out a regulated car finance agreement (a Hire Purchase or Personal Contract Purchase) between 6th April 2007 and 1st November 2024.

You may be able to make a claim if you weren’t told about one of the three following arrangements between the lender and broker:

- A discretionary commission arrangement, where the dealer adjusted variable interest rates to increase their commission.

- A high commission arrangement (39% of the total cost of credit and 10% of the loan).

- Where there was an agreement between the lender and broker, which gave the lender exclusive or near exclusive right to provide credit. However, contractual ties won’t be included if there were visible links between the lender, manufacturer and franchised dealer. For example, where they shared a common or similar name.

Equifax can't determine or advise on making a claim, but our Car Finance Checker can provide you with your motor finance history so that you can contact your lender directly to enquire.

The FCA states that higher interest rates are not due to being mis-sold car finance, but as a result of an 'unfair relationship' between the borrower and the lender. You can view your motor finance history via our Car Finance Checker once you download our app.

Simply input a few details, and our records dating back to 2007 will surface, allowing you to gather all details needed to ensure you find your finance agreements that may fall under the motor finance redress scheme.

Once you have these details, you can then contact your lender directly.

The FCA has granted an implementation period for lenders and timeframes can vary depending on whether you raise a complaint and when you took the motor finance.

- If your agreement started between 6 April 2007 and 31 March 2014, and you complain before 31 August 2026, you should hear by 30 November 2026 at the latest.

- If your agreement started between 1 April 2014 and 1 November 2024 and you complained before 30 June 2026, you should hear by 30 September 2026 at the latest.

These timeframes are different if you do not raise a complaint. Please see the FCA website for further detail.

No, this scheme also covers compensation for vans, motorbikes, or campervans on PCP or Hire Purchase between 6 April 2007 and 1 November 2024.

Equifax is not a car finance lender and is not part of the motor finance compensation scheme. If you think you may be eligible for compensation or wish to make a motor finance complaint, you do not need to contact Equifax.

If you wish to raise a complaint regarding the commission arrangement of your motor finance agreement(s), your next step is to contact your lender(s) directly. The FCA has confirmed that you do not need to use a Claims Management Company (CMC) to do this.

Please see the FCA website for further information regarding the redress scheme: https://www.fca.org.uk/consumers/car-finance-complaints

Please select your finance agreement from the 'Motor' section on the myEquifax App to view the details of your agreement. If you scroll to the bottom of the screen you will find a link to your lender's website.

If you wish to contact a lender that is not displayed on the myEquifax App, please search for your lender's website using a search engine.

While Equifax aims to provide a complete view of car finance data, it is important to understand that the information displayed in the app is entirely dependent on the data reported to us by third party lenders. Some lenders do not share motor finance information with us.

If you do not see a specific motor finance agreement, it is likely because the associated lender does not participate in data sharing with Equifax.

Additionally, an agreement may not appear if it falls outside the current date range for the proposed scheme. The app only displays motor finance agreements taken out between 6 April 2007 and 1 November 2024. For loans taken out post 1 November 2024 these may show on your credit report but not within the motor finance section of the app.

For up-to-date information on FCA guidance regarding car finance claims, please see the FCA website.

Equifax is not a car finance lender and is not part of the motor finance compensation scheme. If you think you may be eligible for compensation or make a motor finance complaint, you do not need to contact Equifax.

If you wish to raise a complaint regarding the commission arrangement of your motor finance agreement(s), your next step is to contact your lender(s) directly. The FCA has confirmed that you do not need to use a Claims Management Company (CMC) to do this.

If you cannot locate your original contract, there are several ways to try and find the details of your agreement:

- Review your credit file: If the agreement was active within the last six years, the information should be present on your credit report.

- Check old bank statements: Look for recurring monthly direct debits to identify the lender.

- Contact the dealership where the vehicle was purchased.

If you know who the lender was but do not have the exact agreement numbers, you can still submit an enquiry or complaint. Lenders are required to attempt to locate your records if you provide key identifying information such as your name, past address, date of birth, and vehicle registration.

When Equifax receives personal data, we perform many checks on it to try to detect any defects or mistakes. Ultimately, we often rely on the suppliers to provide accurate data. If you think that any personal data Equifax holds about you is wrong or incomplete, you have the right to challenge it.

Please note that for data relating to any archived motor finance data, e.g. loan agreements closed more than 6 years ago, you should refer to the Lender directly.

Is your agreement active / closed within the last 6 years?

- If yes, please use this link Online Help to raise a data dispute.

- If no, please refer directly to your lender. Contact details may be viewed in the motor finance section of the app.

The car finance agreement information we hold in our database spans a number of years. Therefore, you might not recognise the name of the lender associated with an older agreement. This may occur because:

- The lender may now be operating under a different name (rebranding).

- The original lender may have been bought by another company.

- The original lender may have sold your agreement to a different company.

To confirm the identity of the car finance provider, you can check the Financial Conduct Authority (FCA) Register, where you can search the name that appears on your records to see their trading names and previous names.

To share/download the agreement information, select it within the app and use the share icon. You can then send it through email, messaging apps, Google Drive, or cloud storage.

Your credit report is not currently available in the app but we are working on adding it over the coming months. In the meantime, please use this link to direct you to your Credit Report.

Your Equifax Credit Score is calculated using the information held within your credit report. To understand your Equifax Credit Score, you should first access your full Equifax Credit Report. You can do this by selecting the ‘view your statutory credit information’ link within the app.

For general information about how to maintain a good credit score, visit: https://www.equifax.co.uk/resources/loans-and-credit/how-to-maintain-a-good-credit-score.html