Credit Hygiene

Credit scores or credit ratings are used to assess an individual’s credit worthiness. A good credit score could indicate that you are good at managing money, and/or that you are financially stable, whilst a poor credit score can imply the opposite.

When you apply for any form of credit, lenders may use their own credit score to determine whether you are a suitable applicant. If your credit score is low, credit providers may be less likely to give you the loan or credit if they believe you will be unlikely to meet repayments. Some lenders may grant a loan with a low score, however, the amount you will be required to pay back can be higher to offset any perceived extra risk.

There are a number of things that can affect your credit score. Missing credit card or bill payments may negatively affect your score, which could lead to a rejected credit application. However, keeping up payments on a credit card, choosing carefully when you apply for credit, and cancelling unused credit cards may help to improve your score.

{kind=link}

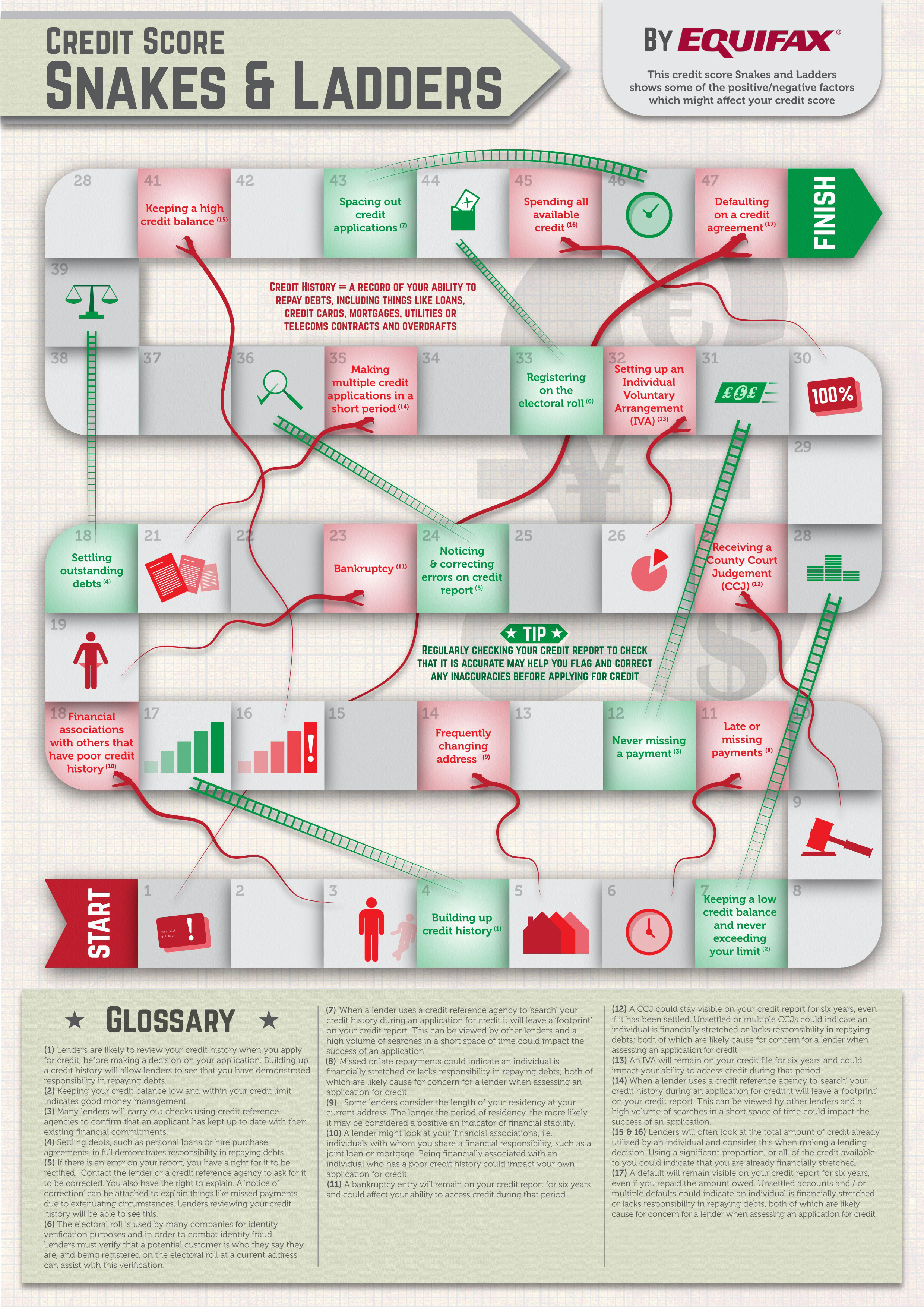

Credit Hygiene

Organising your financial life can be challenging if you have a poor credit history. If a bank believes that you are unlikely to repay borrowed money, applying for credit such as a mortgage can become very difficult. Maintaining good credit hygiene is therefore important, and the following points can help you do this:

- Making payments on time – Missing payments on a mortgage, loan, credit card, utility bill, or other financial arrangements can reflect poorly on an individual’s credit score, and can stay on the record for six years or more.

- Settling outstanding debt – Banks and credit card companies may be reluctant to lend money to applicants that already have sizable debts close to, or at their maximum limit, as this can imply that the person is financially stretched.

- Limiting credit applications – Credit applications leave a ‘footprint’ on your credit report. Too many in a short period of time could negatively affect your score and impact the success of an application as it may convey a level of desperation to lenders

- Avoiding cash withdrawals from your credit account – Withdrawing cash or cash advances from a credit card will be identified by looking at your credit report. Lenders may look upon this unfavourably as it could indicate poor money management.

- Establishing credit history – Your credit history can show how you have managed your money in the past, and may be used as a basis for how you will do so in the future. Few credit agreements in the last 6 years may make lenders cautious about lending credit because there is no demonstration of responsibility in repaying credit. A credit history can start with a simple mobile phone contract or becoming a payer on a utility bill.

- Registering to vote – Lenders can use the electoral roll to verify a person’s identity and as an independent source to confirm you live at the address used on your application form.

- Keeping credit reports in order – If there are mistakes on a credit report then you have the right to rectify it, which can be done by contacting a credit reference agency or the lender. A ‘Notice of Correction’ can be used to explain mitigating circumstances, and will be visible to lenders viewing your credit history. Checking your credit report monthly to ensure the information is correct can be beneficial before applying for credit as lenders update their credit checks every month. You can find out more about Notice of Corrections here.

- Keeping a low credit balance – Using a large portion or all of the available credit can imply to lenders that you are already financially stretched, and may affect future applications. A low credit balance can indicate good money management to lenders.

- Closing unused accounts – When assessing a credit application, lenders may look at the total of unutilised credit available to you.

This article was updated in April 2021; all information was correct at the time of writing.

Related Articles

- Hard vs Soft Credit Searches

- Can Renting Improve Your Credit Score?

- Guide to student overdrafts

- Guide to student credit

- What is a credit blacklist?

- What Is A Cash Advance?

- What are 0% interest credit cards?

- Moving to the UK and your credit score

- Who can see your credit report?

- Should you lease or buy your next car?

- Student loan repayments

- Balance transfers explained

- Credit cards and minimum repayments

- Financial association explained

- Getting a mobile phone contract with bad credit

- What is a credit union?

- Why have I been refused a credit card?

- Why do people use vehicle refinancing?

- What does my credit score say about me?

- What to do if you've missed payments

- New interest rates for savers and borrowers

- How to maintain a good credit score

- Can you achieve the highest credit score?

- Can you pay off loans early or late – or take a payment holiday?

- Infographic: Back to basics – how do credit reports and scores work?

- What happens to credit history when moving abroad

- Credit checks for renting

- Understanding credit score ranges

- Divorce and your credit score

- How credit cards work – how they may affect your credit rating

- Students and credit reports

- Credit agreements – the basics

- Different types of credit card

- Death and credit reports

- Newlyweds, financial planning and credit

- Getting credit cards with bad credit history

- What is a guarantor and how do they work?

- Explaining compound interest

- How Credit Scores Affect Car Finance

- How can I improve my credit score?

- Getting credit with no credit history

- Soft credit searches explained

- What to consider when applying for credit cards

- What is a credit rating?

- What types of credit can you get?

- Staying on the electoral register when moving

- The Electoral Register and How It Influences Credit Scores

- 7 types of credit provider

- Electoral Roll Guide

- Credit: Why do People Use it?

- Credit Myths - The truth about Credit

- Interest Rate Types

- Which factors affect credit scores??

- Your Credit Limits: Do’s & Don’ts

- Secured Vs Unsecured Loans

- Joint Liability - Everything You Need to Know